[Update (again) Since 2015, the L$ Authorized Reseller Program has been cancelled]

[Update 2013/05/07 6 PM GMT — Linden Lab has just announced the launch of the Linden Dollar (L$) Authorized Reseller Program]

Software features turn into products

Nine years ago, Linden Lab revealed a series of new features for Second Life® which would dramatically change the way we think and interact with this virtual world. One was user-generated animations — before that, we were all stuck with a handful of ugly or hilarious Linden animations and couldn’t change them (but there were some creative attempts to mix and match them with some entertaining results).

Another was XML-RPC. This was the first “instantaneous” way of communicating with external Web servers from an in-world object and getting a response almost immediately (previously, you could only communicate via email). Although this was a very geeky piece of technology, it meant that suddenly you could interface Second Life to pretty much anything out there which could run on a Web server.

Two applications became grid-wide famous. The first was the Gaming Open Market: it was the first currency exchange for Second Life (and several other popular virtual worlds and games). The idea was simple: people having L$ in excess could place them for sale on GOM, and whoever was interested in getting those L$, would announce a price in US$ for those L$. Of course, everything was anonymous; GOM would just act as an electronic mediator, exchanging L$ between seller and buyer inside Second Life, and exchanging US$ between buyer and seller outside of it.

When we think about “currency exchanges” — and certainly this is the idea often conveyed publicly — it looks like somehow L$ are transformed into US$ or vice-versa. Even to someone who is much more familiar with how exchanges work, there is this idea that somehow, physically, L$ cross the wire and are turned into US$ and vice-versa.

But a currency exchange is much simpler. What happens is simply that a seller of L$ can say to a friend: “I’ll pay your avatar L$ 1000 if you give me a US$5 bill”. This kind of thing can happen all the time. You don’t need any technology for that, just someone willing to send L$ to another avatar and happy to accept some US dollars (or Euros…) in exchange. The L$ never “leave” the virtual world. They don’t “exist” beyond it.

What GOM did was just automate the process. Instead of avatars running around in Second Life looking for people willing to give them real US dollars in order to send someone else’s avatar a few L$, the whole process was much more easily accomplished, by transferring the money to a central authority (a master avatar for GOM), and announcing — anonymously — the offer on a website. Interested parties would only need to log in, see what was being offered, and pay US$ to the system. It would automatically handle the L$ transfer to the buying party.

As you can see from the 2004 article by Daniel Terdiman, who used to be a very prolific writer about Second Life, Linden Lab was drooling with the idea. Shortly thereafter, the very same process of communicating with Second Life prompted Apotheus Silverman to launch something very similar. If people were willing to go to a website and pay for L$ to transfer hands, would they do the same for content to change hands? That was the basis of SLExchange, which in turn became XStreetSL, and was finally absorbed by Linden Lab, who turned it into the SL Marketplace we all know. But the original name — SLExchange — points to the original intent: it was also going to work as a currency exchange and compete with GOM. In fact, they did, for a while, do exactly that.

Then GOM was crashed by LL, after years of successful business, and LL had very quickly to come up with the LindeX instead. At the same time, many others started their own exchanges, as well as web-based virtual goods marketplaces. Casinos, gambling, banking and investment funds came very shortly thereafter; all relied on very similar principles, at least from the technical point of view.

The first financial crisis: shutting down gambling, online casinos, financial investments

Within time, Linden Lab starting shooting their own foot. I can only attribute that to paranoia because that’s the kind of irrational behaviour driven by fear. They “feared” that they would be liable for people losing money invested in all those third-party services, even though Linden Lab had nothing to do with them. Remember that the L$ never leaves the virtual world. It doesn’t exist outside of it. All that happens on these external websites is that you get to remotely control to whom the L$ are being transferred — from a bank’s avatar account to a customer, for instance.

But LL feared this liability so much (perhaps scared by their own incompetent lawyers, or the dangers of microgaming for free) that first they shut down casinos and gambling, and shortly thereafter, re-classified banks and investment funds as “gambling” (which is ironical — I also agree that they are “legalized gambling” in most countries, but Linden Lab had at least the courage to label it that way and shut them down!), and closed them down as well.

All of a sudden, over 15% of the virtual economy simply disappeared overnight. It was a serious blow, which took years and years to recover. The rate of economic growth never became as steep as it was before the gambling/banking shutdown. And, in fact, although the economy did eventually recover, it was a bit too late: the landmass already started to shrink very slightly.

Day-trading is part of economic life. Depending on your political views, you might dislike others to get rich through their skills and perception at cleverly manipulating the exchange rates, but it’s hard work nevertheless, and high risk — which sometimes pays off. It’s “legalized gambling” again, and, as such, it also gives an adrenaline kick which the day-traders obviously enjoy. But nobody would have heard about Bitcoin if the day-traders hadn’t been wildly speculating on the Bitcoin exchanges.

Bitcoin: a speculator’s dream come true

Let’s be honest. When was the last time you bought something with Bitcoin? Seriously. Unless you’re an open-source ultrageek or a right-wing libertarian, it’s very unlikely you have ever heard about Bitcoin outside the drama on the news — while probably logging in to Second Life every other day to buy a few new outfits for your avatar and pay the rent of your parcel, and never came across the word “micropayment” or “virtual currency” before.

If you do a search for “Bitcoin” on Google, most of the websites out there will be exchanges — not companies providing services that you can buy with Bitcoin. Why? Well, the biggest interest in Bitcoin is, indeed, speculation. As this Forbes journalist found out, it’s not very easy to live a whole week only spending Bitcoin, but it would have been much harder (if not impossible) one year ago.

Why is Bitcoin so popular among traders? It’s not only the issue about the media hype. There is a psychological thing running in the back of their minds: Bitcoin feels to have value beyond the exchanges because you require a huge amount of CPU to generate new Bitcoin. So, in a sense, CPU power is a limited resource, and the available CPU power for generating Bitcoin gives it some value. It makes sense.

Remember that the problem with virtual currencies is… who backs them up? Who vouches for them? If you want to step outside governments and established banking institutions — which pretty much all of them want to do — the question is always, “who vouches for the currency?” Bitcoin’s success comes probably from the idea that there is no organisation behind it, but that Bitcoin has value because they represent CPU power.

Other companies, fully knowing that they would have to face the problem of respectability and credibility, tried to base their virtual currencies on gold (or similar valuable assets). The idea would be that, if anything went wrong, at least you could always sell the gold. This is pretty much the model envisaged by Neal Stephenson in his romance Cyptonomicon — a digital currency based on gold using cryptography. Unfortunately, all these companies were closed down due to some sort of fraud or criminal activity (including murder!).

What else is left?

A microcurrency for the mainstream

If a company like eBay, Amazon.com, Apple, IBM, Microsoft, Google, Samsung, Oracle, etc. would launch their virtual currency tomorrow, we would certainly accept it — especially in the cases of eBay and Amazon.com (and, to a degree, Apple and Google), because we know they have lots of users already in a marketplace buying and selling goods (physical in the case of Amazon and eBay — although they also sell digital goods, of course — and digital in the case of Google and Apple). So, very similar to what countries base their value on, this would be a currency based on the solidity of a market: the number of transactions, of buyers and sellers, and so forth. It would be a huge success.

Sadly, however, none of these companies is interested in developing that.

But here we have Second Life. A marketplace for digital goods with a decade of existence, with 34 million registered users, a million of which engage actively in buying and selling digital goods — and using a virtual currency for that. It’s worth a bit over half a billion US$ annually — not something to disregard. Even though the currency exchange is relatively free, Linden Lab has some interesting way of controlling it: they buy and sell L$ as well to keep the exchange fluctuating widely — a plague that haunts Bitcoin. Not so with the L$: it’s quite stable, and has been so for a relatively long time.

The beauty of the L$ is that you don’t need to “trust” Linden Lab to keep it valuable. All you need is to have a whole huge marketplace with over 6 billion goods and services, and consumers willing to buy them. That’s what gives value to the L$ — and not Linden Lab, not even how much Linden Lab makes with Second Life (which is far less than what the virtual economy is worth).

Now if I had all this in my hands, what would I do?

Expand. To the whole world beyond the boundaries of a puny grid and a limited user base.

When Philip Rosedale announced that Coffee & Power was to accept payments in L$, this seemed to be the first sign in the right direction: turning the Linden dollar into a ubiquitous means of payment for services bought and sold over the net. Philip still maintains good relationships with eBay, Amazon.com and PayPal, and, if Coffee & Power became a success, we might have seen the Linden dollar making an appearance over there. Imagine what that would mean — e-commerce is worth thousands of billions every year, and a fair slice of that comes out of Amazon.com and eBay. It’s clear that the Linden dollar would get a huge boost in importance.

But even if it grew modestly, it would still become a serious “competitor” as a virtual currency. And who would be the first ones to benefit? Why, OpenSim users, of course. One of the reasons VirWox was so successful at the beginning is that they allowed L$ to be exchanged for currencies on affiliate grids (another reason, as we will shortly see, was the ability to accept lots of different ways to transfer money, as well as charging lower fees than the LindeX). But, of course, not all grids are “affiliated” with VirWox; most prefer to create their own currencies instead (just for greed — as if they had any chance of succeeding with that closed-minded approach…). Still, if Linden Lab exposed an API allowing L$ transactions, I’m sure that most grids would accept the L$ as well.

And so would third-party marketplaces. Or the equivalent of things like Flattr and Kachingle might be created using the L$. Why not? It’s such a convenient virtual currency for micropayments.

The current crisis: too many residents cannot use PayPal

So what would the next step for Linden Lab be? Well, of course, the first thing is to start accepting more ways of converting real currency into L$ and vice-versa, beyond credit cards and PayPal. I believe the only reason why they don’t do more — they have been delaying that for a decade — is that day traders, who move a lot of money through the LindeX, probably don’t care much more about other ways of payment. And LL, to accept more forms of payment, would need to establish more contracts with payment gateways, and probably have to set up a different fee system to deal with those payments. It might simply not be worth all the trouble. If 95% of all LindeX orders (which, of course, pay fees to LL) come from customers perfectly happy with PayPal and credit cards, why should Linden Lab bother?

Hint: VirWox makes half a million US$ in transaction fees from people who are not able to use credit cards and/or PayPal and/or are unwilling to go through the LindeX. But mostly from residents who have no other choices, because LL doesn’t give them those choices. So how many are there?

Wolf Baginski, commenting on Inara Pey’s Living in the Modem World, says:

“The turnover for Virwox is pretty big. Their trading volume for 2012 was 9.6 billion L$, which is roughly 38 million USD, and their spread is about 1.6%. That’s half a million dollars that LL doesn’t see. Sounds a lot, but compared to the annual total for tier it’s not so much. Still, it’s a motive.”

Half a million doesn’t sound like much, but Inara Pey points out that this extra money would go a long way to close the gap from losses due to decreasing tier. So Linden Lab is missing an opportunity.

Once this issue is resolved, and LL starts accepting more sources, then, well, the next step is to become a fully regulated virtual currency operator. They are almost one.

Now I don’t even pretend to understand how the applicable legislation works, much less how it applies globally. There is a good reason why money transfer operators (like PayPal) have to open delegations in several different countries, to be able to transfer money around the world: as legislation changes from country to country, to be able to deal with them all, it requires fully licensed organisations in each country where they operate from.

Personally, I think this is absolutely insane, but more on that later. Money printing is a business. It’s obvious that “those in power” want to control who is allowed to print money. It’s unavoidable. But they want also to protect consumers from fraud.

Becoming a MSB

So, at this point, Linden Lab has basically two choices. The first is to grab the opportunity: they have a very rare virtual currency, one that is backed by a thriving economy worth half a billion US$ annually, and which already has millions of users. They have far, far more than PayPal had when PayPal went international — and PayPal doesn’t even offer a virtual currency, just an easy way to send money around the world.

But this allegedly requires a lot of bureaucracy. Because of the paranoia of money laundering, the burden is apparently placed on money sending institutions to spy upon their customers, see what they are doing, and report everything — and allegedly this cannot be even automated easily, but really requires humans typing on Excel spreadsheets. That is costly. In fact, too costly for Linden Lab — assuming, of course, all this is “true”.

Of course, as we should easily predict, Linden Lab is just doing precisely the opposite: shutting everything down.

Inara Pey reasons that “something serious has happened”. Even though for about a month or so, she had already noted that the changing legislation in the US has made the strange wording in LL’s ToS pretty much irrelevant — virtual currencies are currencies if they are used as such; it matters little what the currency provider calls them. What this means is that LL cannot “hide” behind their own legal mumbo-jumbo, calling L$ “tokens” and repeatedly claiming in the ToS that they are “worthless” — when they operate an L$-to-US exchange and get an income from it. While I might disagree with the views of the US legislator, I think that at least they’re forcing companies like LL to be honest, disallowing them to hide behind silly wording on a ToS. The new legislation allegedly just looks at the use that is made with virtual currency, not the legal framework (i.e. the ToS) under which the virtual currency is licensed for use. The old adage — “if it walks like a duck and quacks like a duck, it’s a duck” — seems to apply to every virtual currency from now on, no matter what they’re called. Honestly, it makes sense. But from a business perspective, it means that Linden Lab is now a target.

Did they receive a warning from the appropriate authorities or not? It’s impossible to say; LL will definitely never tell us. Hamlet Au, reporting on New World Notes, quotes Vaki Zenovka who claims that LL’s move is to comply with existing legislation. But we can only speculate.

What certainly is the case is that the way they allowed third-party operators to assess risk in transactions with SL residents (via the Risk API) extended LL’s own risk towards companies over which they have no control; most are not even located under the same jurisdiction. So, consistent with LL’s paranoid approach, they shut the Risk API down — and allegedly sent the third-party exchanges emails to tell them to shut their ATMs down, effectively violating their own ToS (which states they have to give, at least, a 30-day warning). The fact is, as Maria Korolov has been telling us on a running report on Hypergrid Business, third-party L$ currency exchanges have been all shutting down in the past few days.

Most did shut down, some ignored it, and apparently two are working with Linden Lab to remain open. An interesting thought, vented by Johnmacloud Jun, CEO from MBKash — who optimistically awaits a reply from LL who allegedly promised a solution — is that Linden Lab might buy some of the now-defunct currency exchanges, effectively “GOMing” them, as they used to do in the past. More on that later.

Not all were closed

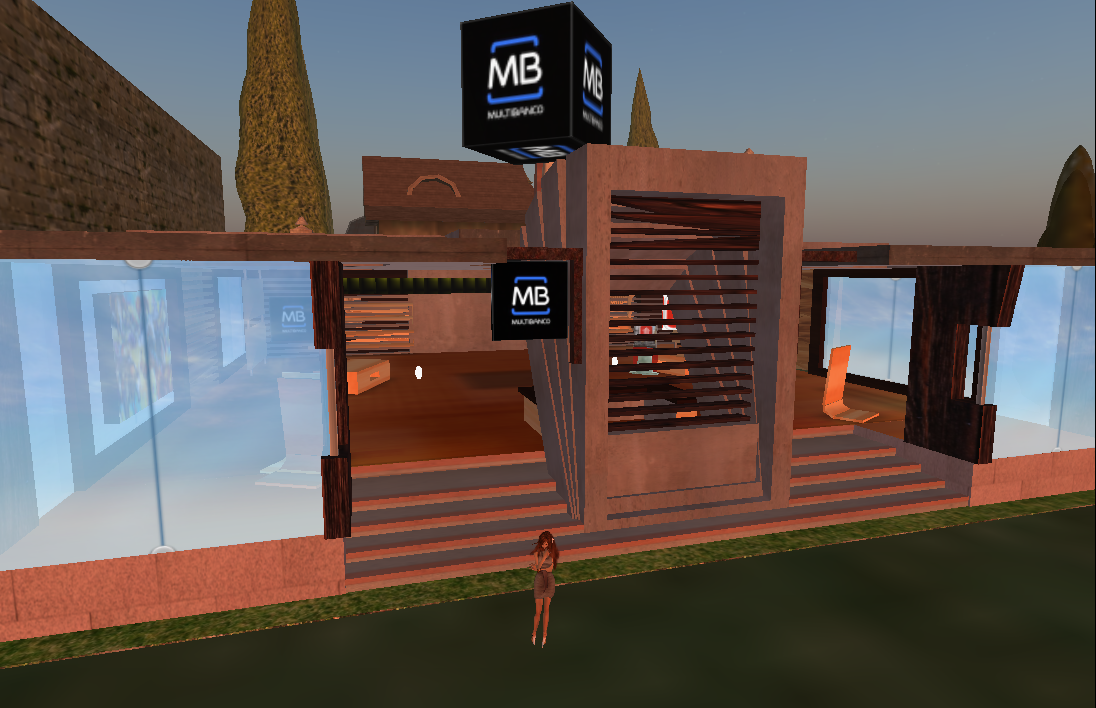

Beyond the most publicly known currency exchanges, I also found two interesting cases that not only completely ignored LL’s requests and warnings, but even started to send customers nice reminders that they are still in operation. Both are Portuguese.

One is Portugal’s ATM network, Multibanco. Don’t take the horrible site as a measure of their importance; Multibanco is a network of ATMs run by the twenty-five largest banks in Portugal, and billions are transferred through their network; in fact, they are so hugely successful, that they absorbed very early in the 1980s all smaller competitors, and are a huge giant in electronic money transfers. Everything that involves digital money transfer in Portugal is processed through Multibanco: from money transfer orders, money communications between individual banks, and the payment of pretty much all services and goods — from terminal payments in shops and restaurants to toll payments, to parking, but including obviously paying for the utilities, for recurring payments, and taxes and fees — all go through them. It’s a tentacular monster that has crept and absorbed anything digital — even Visa, Mastercard, and American Express had to give up their own networks in Portugal and just licensed their operations to SIBS, Multibanco’s parent company.

And since 2007, they also have a Euro-to-L$ gateway, operated by a third party (not affiliated with them, but they started with a special relationship back then — who knows how the situation is today…) Again, don’t be put off by the amateurish website; you’re getting in touch, through a third party, with a payment gateway operated by a company that easily has an EBIDTA of €15 million and a cash value of €100 million. And, contrary to Linden Lab, they have all permissions and authorizations to transfer money in all possible ways, and naturally have an international branch, again fully licensed to operate with currencies beyond the Euro if needed. For them, transacting in L$ is “just another service” in the huge network they operate (until recently, they were also the largest private Internet operator in Portugal, since all their 14.000 ATMs and portable terminals started to use TCP/IP connections). I did cover their services a few years ago (unfortunately only in Portuguese). Their system is very simple: it has a ‘bot logged in to SL. You IM the ‘bot, and it will reply with a reference code, which you can use to pay on any ATM or homebanking system in Portugal. As soon as the transaction is cleared (which usually just takes a few seconds), you get the L$ delivered to your account. You don’t need either SL-based ATMs nor registrations on fancy websites, nothing. There is also a certain amount of privacy: the gateway system knows your avatar name, but all it generates is a payment reference, which is not tied to any account, card, bank, or has a person’s name or ID anywhere on it. It’s just a sequence of numbers and an amount. On Multibanco’s site, they will obviously know what card and bank account is used to pay the reference, but they have no clue what the reference is for — they will most certainly have no idea what avatar will receive the L$. It’s a blind system.

There is a competing payment service in Portugal, which runs independently from the financial institutions: it’s the National Postal System, which obviously also shuffles a lot of money around. They have their own network for service payments, called Payshop. Instead of ATMs, they have opted to partner with thousands of independent small businesses around the country, giving them a small terminal that connects to their services. To get L$ transferred to one’s account, all we need to do is just to go to one of the thousands of agents and ask them to buy some L$. They will accept our payment in cash and emit a ticket with a sequence of letters and numbers. Back at home, there is another ‘bot just for this service (again, using the same third party who also operates the gateway with Multibanco), which we IM with this sequence, and we’ll get our L$ in a few seconds. So it’s even more anonymous. The agent at the shop never knows who we are: we just hand them over a cash payment, and, obviously, we don’t need to give our names, addresses, ID card, whatever. We’re just an anonymous customer. The Payshop network has no clue who we are; they have absolutely no information on us. For statistical purposes, they can certainly have an idea about which agents have been emitting sequences for L$ money orders, but they have no idea if the same person is buying L$ or if it’s a different person. It’s totally untraceable. And, in-world, the service handing out L$ also have no idea who we are or which agent we visited to buy the ticket with the sequence of numbers. They just redeem the code, clear the transaction, and you get your L$ — you can even use whatever avatar you wish. Let me repeat again: nobody has the slightest clue about who is buying L$ for which avatar.

Granted, both these systems are only one-way, and they are not a “currency exchange” with buyers, sellers, day-traders, or anything fancy which allows day-trading and speculation. LL cannot ask them to remove their in-world ATMs, because there are no ATMs to remove. There are not even any humans involved in this process. And, obviously, LL could ask those people to remove their ‘bots, but the truth is, the ‘bots only exist in order to make the process run 24h/7 without human intervention. These systems are so simple that if LL forbade them to run ‘bots, they could also work with avatars with humans behind them: they would just need to wear a scripted attachment to handle payments. And if LL would also forbid avatars to attach scripted devices to them, well, this could still work manually: the human operator would just need to have access to a website and see who they have to send L$ manually. LL can’t stop people from sending L$ to others!

You see the point I’m making here. We like to think of “currency exchanges” as very complex software which handles authentication, user validation, credit card management, and so forth, and where money is shifted between people according to a price that is fixed by demand and supply. When seen that way, I can understand that it can be viewed as “evil money-laundering schemes” by FinCEN or whatever authorities might be snooping around.

What about the LindeX?

One thing is fearing that third-party L$ exchanges, not being under the control of Linden Lab, may be violating FinCEN regulations by doing fraudulent transactions — and that LL may be implied, for the reason they have created the L$ itself (and now cannot avoid mumbo-jumbo legalese to escape being regulated). In that case, it makes sense for LL to shut them down, as a safety precaution.

But what about the LindeX? Even if it’s the only “legal” L$ exchange, it is still subject to regulation as well. What this means is that LL needs now to employ a vast staff of specialist professionals to do all the required bookkeeping, accounting, and reporting that FinCEN requires — which, allegedly, is insanely hard to do and quite expensive. Does LL have a margin on the commissions they charge that allows them to be fully compliant with the current legislation? Again, we can only speculate. I would guess “no” — unless it means firing developers and hiring accountants and lawyers, and, even so, it would mean operating the LindeX at a loss (or they will have to raise the commissions and fees…).

So there is here an unknown variable in the equation. What will Linden Lab do next, once the third-party exchanges are over and FinCEN agents start knocking at LL’s door? Shut down the LindeX as well?

Hamlet Au did a very simple (and highly inaccurate) survey and announced that 28% of his readers report a moderate-to-high impact in their SL usage. Even if that survey has serious problems, it shows that a rather large fraction of the SL user population might indeed be affected — namely, all those hundreds of thousands of residents who are unable/unwilling to get an international credit card and/or PayPal. So imagine that this means 28% of the landmass, the population, and the economy shrinking. That on top of the 10%-12% of shrinkage that will happen anyway. Suddenly, LL’s execs will need to explain to their Board why they shrunk 40% in a single year — thanks to a badly handled situation.

But imagine that LL has to go “all the way” — namely, shut down the LindeX as well. As some residents have correctly pointed out, the SL Marketplace already allows you to pay either in US$ (via a credit card or PayPal) or L$. Linden Lab might simply stop offering the L$ choice, and pay merchants directly in US$ (minus fees) — which would be similar to, say, DAZ, which operates a marketplace for 3D content without a virtual world.

How much would that impact the whole economy?

Well, for starters, all content creators who are unable to use PayPal would be left out. 28% is a lot of them. Sure, the content creation market is saturated, with little margin for growth, and established content creators would sigh with relief at the loss of a substantial part of their competition. But on the other hand, it would also mean a much smaller market with fewer buyers.

It gets even worse. Many content creators, in spite of being able to accept PayPal payments, might be unwilling to reveal their real names when doing transactions with residents. LL could act as middle-man, anonymising transactions, but that would probably mean more fees. But the biggest problem is that this would also have a serious impact on in-world business: most shops would have to change their vendors to directly accept PayPal payments. This is easy to do — there are even a few vendors already working like that — but it would require lots of more steps, and, of course, make content creators more liable to pay taxes in their own countries of origin. The current model of using the L$ is much better: you can pay all your rent, tier, and expenses in L$, and only pay taxes on the remaining L$ that get converted to real currency via the LindeX. Again, such a measure would mean even fewer content creators willing to offer things for sale in SL.

And because the “PayPal vendor” requires so many more steps, it’s much easier just to deal with the SL Marketplace — thus pushing more content creators to abandon their shops, reduce their land, and shrink the landmass more and more, depriving Linden Lab of even more revenues.

Putting it all in perspective, what this means is that it looks that, no matter what Linden Lab does to remain FinCEN-compliant, they will lose hundreds of thousands of customers (they may remain as residents, of course, but not as economical agents — they will pay LL nothing, and contribute nothing to the economy) and, consequently, reduce LL’s overall income for 2013.

It’s not a pretty sight. What can Linden Lab do?

(Second) Life without the Linden Dollar

The first option is the more obvious one: start immediately accepting new forms of payment. Note that this has been in discussion, to the best of my knowledge, since 2005. Every other year or so, LL actually gets a team to investigate payment gateways, but they tend to abandon the idea. I imagine that they have consistently misrepresented the impact of the third-party exchanges, which have always accepted several different types of payments. Truly, they have no excuse — not even the excuse of “high fees”: at the levels that LL transacts currency, they can do far better deals with payment gateways than any of the third-party currency exchanges, which are already able to accept multiple payment systems and operate charging lower fees than LL. Linden Lab certainly has more than enough developers to integrate those payment gateway systems with their own software!

The only reason for not accepting other payment forms is because LL is stubborn (and, incidentally, because they are probably not aware, or couldn’t care, that everybody who cannot use PayPal and who is happily exchanging L$ for real-world currency have always done so at a third-party currency exchange). Maybe hard facts and reality will make LL finally change their minds about those additional payment methods. This would go a long way to prevent non-credit-card-users to remain in-world, even though it would mean that the third-party exchanges would all be out of business… that is, if FinCEN allows the LindeX to continue to exist.

If.

An interesting suggestion is that, apparently, you’re not subject to regulation if you do not convert virtual currency into real-world currency. I have no way to validate that statement, but it means that there would be an easy way out: Linden Lab could just operate the LindeX with… Bitcoin 🙂 (Sure, they would still have to shut down the third-party exchanges first). That way, you’re just trading a virtual currency for another virtual currency, and that is not (yet) subject to legislation. And, of course, there are gazillions of Bitcoin exchanges out there — most of which are beyond the reach of the FinCEN, and accepting all sorts of payments. In fact, the current L$ virtual exchanges would only need to switch to become Bitcoin exchanges instead and continue to do business as usual (since they already have customers!). The disadvantage? Both the Linden dollar and the US dollar (or the Euro, the British Pound, the Swiss Franc, the Canadian and Australian Dollars…) are stable currencies. Bitcoin is not. It fluctuates wildly. While LL could certainly keep the L$ from fluctuating — as they have so successfully done so far — they would have no way to control the Bitcoin fluctuations. On the other hand, non-US Bitcoin exchanges interested in continuing to have customers could offer a fixed Bitcoin-to-whatever-currency rate — becoming much less a speculating market than a convenient service for customers. In fact, to be honest, I understand little of this virtual currency business, but it looks to me as if there is a good market for a Bitcoin exchange that does not fluctuate wildly but simply that offers a sensible fixed rate… it wouldn’t appeal to speculators, but certainly appeal to people just wishing to convert currencies.

There is a third option, which should have been obvious (it was immediately obvious to Moon Adamant, my clever roomie, who always grasps these things immediately). Linden Lab could just buy a third-party exchange — one not located on US soil, of course.

This seems not to be so far-fetched as it sounds. After all, as mentioned, MBKash’s CEO fears exactly that LL might be thinking of buying VirWox. Why VirWox and not of the others?

VirWox has one interesting advantage: while many of the third-party exchanges are also based outside of the US, VirWox (an Austrian company) has worked in partnership with the University of Vienna to develop the integration with OpenSimulator. In fact, much — not all — of the work to make OpenSimulator support currency transactions, compatible with the SL Viewer, comes from development by academic researchers at U. Vienna. When I first applied to test out their software with our grid, I was actually curious that I got in touch not with a VirWox representative, but with U. Vienna directly, who worked out with me to help me up set up the test environment. This is an excellent example of close university/corporate cooperation, and it would certainly appeal to Linden Lab, now that they are apparently interested in attracting the attention of the academic world again (we all know it’s too late for that — they have almost all moved out to OpenSim already — but it’s still a good sign that LL is not “hating” academics, as they did during M Linden’s time). It also lends some extra credibility to VirWox.

And, of course, it’s also a positive story to present to the media. If someone picks up on the L$ story — “it’s as bad as Bitcoin! People are selling drugs and laundering money in SL!” — LL could simply point out that they don’t run their own exchange, but instead partnered with a serious and respectable European university to run an L$ exchange as an academic project. It is already the subject of several academic papers published by reputable scientific journals.

Surprised? You shouldn’t be. We all know that the hype has left Second Life years ago. However, serious economists aren’t dazzled by hype; they continue to do research in spite of that. But perhaps more surprising than all that is that it’s not just academics in their ivory towers that are doing the research. In fact, the allegedly richest bank of the world (in terms of assets) — nothing less than the European Central Bank (€3 trillion in assets) — has published a detailed report on virtual currencies covering Bitcoin and the Linden Dollar as case studies. While they certainly mention World of Warcraft and Facebook Credits, these concern them little, since these are not “true” currencies in the usual sense of the word (i.e. you can buy them, but not convert them back — legally, at least).

Bitcoin, because it allows buying “real” products, is especially interesting for the ECB. Not because they “fear” the currency, or because it can be used for money laundering or similar illegal activity. The main reason for the whole report to exist is to know how European citizens can protect themselves from fraud, and what recourses they have when things start to go wrong. With Bitcoin, of course, no centralised authority exists, so there is nobody to complain to. They also warn that a total lack of deregulation of the Bitcoin valuation means that users have no way of knowing (or of predicting) how much their Bitcoin are worth one day or the next. Here is a typical quote:

“Chart 6 shows the evolution of Bitcoin’s exchange rate on the Mt.Gox exchange platform during the hours of the incident, and is also the expression of how an immature and illiquid currency can almost completely disappear within minutes, causing panic to thousands of users.” (emphasis mine)

or even:

“All these issues raise serious concerns regarding the legal status and security of the system, as well as the finality and irrevocability of the transactions, in a system which is not subject to any kind of public oversight. In June 2011 two US senators, Charles Schumer and Joe Manchin, wrote to the Attorney General and to the Administrator of the Drug Enforcement Administration expressing their worries about Bitcoin and its use for illegal purposes. Mr Andresen was also asked to give a presentation to the CIA about this virtual currency scheme. Further action from other authorities can reasonably be expected in the near future.” (emphasis mine)

How true! We should all have seen this coming (the ECB report is from October 2012). One of the things that the ECB is worried is about the impact in the real economy of the use of Bitcoin.

By contrast, this is what the ECB has to say about the Linden Dollar (regarding the way LL regulates the money supply and the impact that this mechanism has):

“This money creation process, which artificially inflates the money supply, could be creating a boom within Second Life’s economy that could lead to a recession if Linden Lab is forced to tighten its money supply. In this situation, a loss of confidence and a sudden deprecation of the Linden Dollar would be expected, causing all users that are involved in the virtual community to suffer some losses. In any case, it is important to highlight that this would only have a negative impact within the virtual community and for its users. Its effects would not spread to the real economy.” (emphasis mine)

Note that the artificial inflation by “printing money” which Linden Lab used to do is referred to a published academic article in 2007; LL, since then, has claimed that they don’t really need to “print money”, they can just use a reserve which they sell to the market when needed. The ECB has also considered this mechanism:

“As can be seen in Chart 8, the exchange rate has been quite stable, at around L$ 260 = USD 1. This is because Linden Lab tries to keep volatility low by injecting new Linden Dollars as demand increases. Therefore, it can be said that the Linden Dollar is, to some extent, pegged to the US dollar. […]”

But, of course, the ECB also warns against fraud. It criticizes the way Linden Lab can constantly force users to accept the ToS, and, while it arguably has a DRM system in place, often ignores complaints by users. In fact, the ECB figures out that LL might care too little about their customers, and give them no options to significantly claim their rights. The good side of all this is that Linden Lab is subject to consumer regulation, and, as such:

“Second Life is focused on the virtual world, but this does not mean that everything is virtual in this community. There are real economic transactions behind Second Life and there are also real issues and problems that arise. Within Second Life, Linden Lab is the only authority and regulator. To some extent they also oversee the system, but without the involvement of any public authority. It is not even clear if any authority even needs to be involved. In fact, in the current situation, any potential issue within this virtual marketplace can perhaps be regarded in the context of consumer protection rights.” (emphasis mine)

Why is this important? Remember, the whole point of the ECB’s report is to analyse the situation of virtual currencies, and suggest the role of central banks and legislation in order to protect consumers’ rights. That this is significant even for SL residents can be seen in the history of GOM: allegedly, it was claimed that GOM’s owner has approached LL to help them deal with the issues of fraud. Whatever the reason, it certainly showed that LL did view fraud as one of their main concerns, and, as such, created the Risk API, which all “official” third-party L$ exchanges had to deal with — the idea being that LL was in a much better position to detect fraudulent L$ transactions than the third-party L$ exchanges.

Fraud in Bitcoin is complex to deal with. Yes, of course, you can track all the people that have handled a specific Bitcoin — something impossible with real paper/coin money (including the L$). But, on the other hand, there is nobody to complain to if you are a victim of fraud. Or, rather, you will need to engage in a complex court case just to figure out whom to sue, which might be hard outside the jurisdiction you live in.

By contrast, fraud in L$ transactions is easy to deal with: you just complain to Linden Lab. If LL does nothing, they are liable to all sorts of consumer protection organisations, starting with Better Business Bureaus, and going all the way to suing LL — a well-known company in a well-known jurisdiction. It might be expensive to get justice done, but you know with whom you’re dealing.

Why is the ECB, all of a sudden, so concerned about this? It’s not only them, of course. At least in Europe, central banks are also usually the last resort for consumers to complain about anything related to frauds with financial transactions. So if they simply ignore the existence of virtual currencies, citizens might hold them responsible for not doing anything about it. And, in a sense, they are right: ultimately, at least in those countries where central banks also protect consumers’ rights, they are forced to do something about it, legally speaking. So it’s important that they at least analyze virtual currencies and make recommendations. The ECB certainly has made a lot of recommendations in October 2012 which are quite similar to what the FinCEN has announced in March 2013 (obviously, they talk to each other!). This is a typical warning by the ECB:

“Virtual currency schemes seem to work like retail payment systems within the virtual community they operate. However, in contrast to traditional payment systems, they are not regulated or closely overseen by any public authority. Participation in these schemes exposes their users to credit, liquidity, operational and legal risks within the virtual communities; no systemic risk outside these communities can be expected to materialise in the current situation.”

Interestingly enough, the ECB puts down any fear that virtual currencies might be outlawed:

“Virtual currency schemes visibly lack a proper legal framework, as well as a clear definition of rights and obligations for the different parties. Key payment system concepts such as the finality of the settlement do not seem to be clearly specified. (this refers to the issue that your amount of L$ can be removed by LL at any time, and you have no safeguards in place — either you were lucky to cash out your L$ in time, or you’re at the mercy of LL’s whims). […] Furthermore, the global scope that most of these virtual communities enjoy not only hinders the identification of the jurisdiction under which the system’s rules and procedures should eventually be interpreted, it also means the location of the participants and the scheme owner are hard to establish. As a consequence, governments and central banks would face serious difficulties if they tried to control or ban any virtual currency scheme, and it is not even clear to what extent they are permitted to obtain information from them.” (emphasis mine)

Now, since October, half a year has passed, and, obviously, I haven’t been following financial legislation on either side of the Atlantic since then. What I also found fascinating is the different focus, or emphasis, on American texts on the subject versus European ones. The American texts — at least from the perspective of a European reader! — seem mostly concerned about illegitimate uses of money and how to prevent people from committing crimes. This reflects much more the focus on “do whatever you wish, so long as it’s not illegal”, which is typical of common law systems. The European texts are mostly concerned about consumer protection: if something goes wrong with your virtual currency, where can the consumer complain about the transaction? Thus the need for a framework that protects those consumers’ rights — while leaving criminal activity for the judiciary branches to sort out. This, of course, is not to say that Americans have little consumer protection, rather the contrary; I would even dare to say that the BBBs are one of many examples of how self-regulation actually protects consumers’ rights far better than complex legal European frameworks. “The client is always right” is an Americanism that was just belatedly adopted in Europe; we’re more fond of applying the maxim “The client always has rights” (in the sense of having legal rights to protect them).

So if Linden Lab is truly planning to acquire a European currency exchange to avoid scrutiny by the FinCEN, they will have to take that into account. On one hand, they might worry little about preemptively prevent crime: that’s not their role as a commercial company, they just have to be prepared to help the police with their inquiries (as the British are so fond of saying!) if a crime is being investigated. The measures they already have in place are more than adequate for that. On the other hand, they have to worry much more about consumers’ rights. And this means no more changes to the ToS. It means no more seizing an avatar’s assets (without a court order!). It means following up DMCA claims instead of ignoring them. It means no more sudden changes without warning. It means no more pretending the residents don’t exist and don’t have opinions so they can be ignored. It means no more excluding certain residents from participating in the economy (because they are unable to use PayPal/credit cards). Fundamentally it means no more ToS which removes customers’ rights (which LL is so fond of doing!).

Putting all that in perspective, I seriously doubt LL’s ability to comply with all that — it goes against their corporate culture! In fact, they’re much better off complying with the FinCEN’s recommendations and hiring a whole staff of specialized accountants and lawyers to do all the bureaucracy demanded by FinCEN to keep the LindeX operational.

Of course, there is the last possibility, which is to close the LindeX and not buy VirWox, but just let people know that they are allowed to do transactions with them — even though they’re not “sanctioned” by Linden Lab. This would place the burden of respecting consumer rights on VirWox (as a European company, they are probably better adapted to do that anyway) while still avoiding the FinCEN, by very rightfully explaining to them that they do not operate an exchange in US soil, nor do they own a subsidiary outside the US. But if they follow that route, there is no point in blocking access to any non-US third-party exchanges — they could all continue to exist without endangering LL’s legal position in California.

It would probably be the best choice.

Whatever the reason, Linden Lab is certainly fond of creating its own financial crisis. It’s enlightening to see what Philip Rosedale did think about all this, back in 2005:

“We do NOT have any intentions of restricting other sites or residents from selling currency – we think that a competitive market for currency sales totally makes sense.”

— Philip “Linden” Rosedale, Town Hall Meeting, August 30, 2005

{kind=link}

{kind=link}

{kind=link}